The 3 best places to save your money

Hi! Happy almost-Friday <3 I’m on my way to Zumba and barre at the beach, and have a very special guest post to share today. As longtime readers know, my undergraduate degree is in Finance. While it’s not something that I use now for my career -example A: I’ll be dancing today by a 60 ft. inflatable cranberry- it is something that has helped me immensely with our personal finances and blog endeavors. Even though it’s not my career, Finance is still one of my hobbies, and I enjoy keeping up-to-date on current market stats and working on our family budget and investments. Needless to say, I was really excited when Rachel offered to write a guest post with saving advice for the blog. While this isn’t within the general scope of my usual blog topics, I think it’s fun to branch out, and this is valuable information many could use. Rachel majored in Finance and currently manages corporate development and financial modeling for an education technology company.

Here she is with some tips and strategies to take your savings to the next level!

Hi Fitnessista readers! I’m Rachel and I blog over at The Day Tradette, a site dedicated to making personal finance and investing accessible and interesting for everyone. I write about budgeting, investing ideas, stock market trends, and even ways to save money shopping. My goal is to show everyone, even if you have no finance background, how to maximize your money!

I’m so excited to be sharing my thoughts with you all today! I’ve been reading The Fitnessista for years and it was one of the blogs that inspired me to start writing.

It’s pretty much personal finance 101 that saving your money is important. Duh, Rachel. The thing is, I get that with car and house and gym membership payments to make now, and retirement so far away, putting money aside can feel overwhelming and irrelevant.

But now is the perfect time to save, while you have time for your money to build up (thanks to something called compound growth). All you really need to know about compound growth is that it makes extra money appear, because it’s interest on top of interest. This means even small savings now can turn into a big pile of cash after a while.

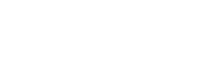

Check out what happens if you put away $100 a month. It may take budgeting work (and I love talking budgets if you ever want to discuss) but think of it like just $25 a week. Depending on where you put it and what returns it makes, you could be sitting on a big pile of cash after 10 years of savings.

Hopefully my wonderfully colored chart convinced you saving is important and we can move on to the fun stuff: how to actually make that extra cash appear. Here are the three places (in order of priority) you should be storing your cash to maximize your savings.

1. A retirement account

Retirement accounts come in two forms: a 401k and an IRA. Both accounts offer tax benefits and are much simpler than they sound, which is why they’re #1 on my savings list.

If your employer provides a 401k, I would choose it over an IRA. Many employers will match a portion of your contributions, and if they do, you should contribute as much as they will match. That’s free money!

Even if your employer doesn’t match anything, it’s deducted from your income on a pre-tax basis. So you pay no taxes now, and are only taxed when you take the money out during retirement. On top of that, a 401k requires zero self-discipline. The money is taken out before you get your paycheck, so there’s no temptation to spend it on something else.

If your employer doesn’t offer a 401k, you can set up an IRA through a broker like Fidelity. Most likely you are getting taxed at a higher rate now than you will be when you’re retired, so a traditional IRA (not a Roth IRA) would make the most sense. You can set up automatic contributions to your IRA too so that you don’t even have to think about it.

2. An emergency fund in a high yield savings account

An emergency fund is important if the unexpected happens – it’s a stash of money you set aside just in case you lose your job, need car repairs, etc. That way you don’t have to worry about debt on top of a bad situation.

Most guidelines call for setting aside around 3 months of living expenses, but exactly how much you decide to put away depends on your comfort level. Think of this fund as letting you live your life with a little less stress.

You need a place to store this money that gives you some interest but also will allow you to withdraw money at any time. I recommend keeping your emergency fund in a high yield savings account. I use the Synchrony Bank Optimizer Plus account, which offers a 0.95% annualized interest rate – the highest I’ve seen.

To avoid temptation, I chose an account password that isn’t in my usual password rotation and would be hard for me to remember. So if I want to withdraw money, I have to call up customer service, which is such a pain I would only do it in emergencies. If you have better will power than I do, feel free to skip this step. 😉

3. The stock market

This one might be a little controversial, so bear with me for a bit. Yes, the stock market is volatile. But if you keep your money in the market for enough time (totally do-able if you start investing young) you will make money in the long run.

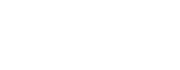

Check out this chart of the S&P 500 index over the past 40 years (the S&P 500 index is a mix of 500 of the biggest stocks, and is used to represent the entire stock market). Even if you invested your money in 2008, right before the recession, your investment would be profitable today.

(Eesh 2 charts in a post – chart nerd alert).

You can totally benefit from the stock market too if you make low risk investments. I recommend starting out by investing in index funds (just like the chart above) that track the entire market. That way you don’t have to worry about picking the company that goes bad.

All you have to do is set up a brokerage account (I like Merrill Edge because it has low commissions) and buy shares of an individual index fund like SPY. If you want something even easier, you can set up automatic deposits in a website like Betterment (link gets you 30 days free) that invests in a diverse range of indexes for you. Betterment does charge fees though and automatically invests regardless of how the market is doing.

Your safest bet is keeping your money in indexes, but you can also put your money in individual stocks if you get more experienced with investing. Focus on companies that are stable, have been around for a long time, and that interest you. Stocks I like for that include Apple, Disney, and Nike. Plus, it’s nice to think you’re investing in your returns at the same time you pay for new running shoes.

If you have more questions, please check out my blog, find me on Twitter, or shoot me an email at thedaytradette@gmail.com. Thank you for reading and thank you again to Gina for giving me the opportunity to share with you all!

Disclaimer: The information presented is based on my personal opinion and experience, and should not be considered professional financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation.

so many great tips! I REALLY need to work on my budgeting skills. This has inspired me to get started today!

Very helpful tips! I feel budgeting is a constant work in progress and I am always looking to improve. Thanks Rachel!

Great guest post! Besides healthy living, my husband and I struggle with a budget. Between a house and 2 car payments are some hefty student loans! You would think an accountant and a finance major would be able to balance our budget…. definitely will be checking out your blog Rachel!

Great tips!!! I am still trying to learn my way with money and these help!

Wonderful post! I’m lucky enough to have a father and boyfriend interested in finance and both have offered many tips as far as money management. It’s crazy that so many young adults are uninformed – I certainly don’t know everything either! It’s great to get the word out, especially for us women!!

This is great, I’m glad that you decided to branch out – would love to see more posts like this. I’d like to add a tip – for my emergency fund, and other various savings goals, I use SmartyPig. 1% interest rate, and very user-friendly and easy to use. I discovered it a few years ago and it has been a fantastic savings tool.

Again, great post. And I think you could write a few yourself, I enjoy seeing how others budget and save.

Lastly – I cannot wait to make those lava almond cakes. And it will save $ rather than getting dessert out. Personal finance win!

Hello! I was super excited to read this post today – I am a Financial Advisor and absolutely LOVE working with fellow young women and helping them realize how much power they have to create the future they want for themselves.

I am always so wary of “blanket” financial advice — everyone has a different situation, and therefore I strongly believe there is NO one-size-fits-all mentality when it comes to saving or, more importantly, investing. One thing that isn’t mentioned in this post and I think is SO SO SO important, is the value that sitting down with someone who is a professional advisor can bring to someone’s situation. I could list a lot of reasons that I don’t believe index investing is a good fit for everyone — or reasons that I would recommend a Roth IRA over a traditional IRA – and a LOT of reasons I would never encourage someone to invest their money in the stock market without any real knowledge or understanding of how it works — but without knowing a person’s full picture, I would feel so uncomfortable making a recommendation.

Granted, I’ll be the first to admit that financial professionals don’t always have the best reputation (And unfortunately, that is with good reason) but speaking from where I know I come from in a client meeting, there truly are people who want to help you, and can provide a service that will prove to be invaluable as you accumulate wealth and approach retirement.

So, I would encoruage readers to ask around and find a financial professional they can trust to help them wrap their minds around planning for their financial future. In the same way that you would never live soley by trying to Web-MD diagnose yourself, why would you trust your financial future to simply your own means? You’d be limiting yourself (and potentially harming the outcome). It is very important to do research and ask a lot of questions to make sure you find someone you would want to work with and can trust — but if you can find someone, it can make such a positive impact on your financial health.

Great topic, Gina! So important and usually so ignored until we’re much older 🙂

I’ve been thinking about doing this, as my husband and I are newlyweds who are looking into buying our first home, and I want to make sure our finances are in check. Would you mind advising what the general costs are of having a financial advisor? Anything we should keep in mind when getting one (credentials, etc)?

With my team, we don’t charge anything for sitting down with clients. The only time a fee or charge comes into play is when we are investing the money (and then that cost varies depending on the type of account and kind of investing we are doing).

There are a variety of certifications advisors can have – depending on the firm, the licensing requirements can vary. (For me, I am licensed with three different securities licenses, along with health, life and long term care insurance).

The Certified Financial Planner (CFP) designation is the result of additional training /testing, and that can definitely bring added value to the table, although is not required, in my opinion.

You shouldn’t run into cost to sit down with someone – but it’s obviously good to check before you meet 🙂 The most important thing is that the values and philosophy of the person you consider working with aligns with yours, and that you feel comfortable!

Great post! I rely on my husband a lot for our own savings and budgeting since he works in finance but I do try to stay on top of things and understand where my own money is going and how to save better!

I don’t understand how to get involved in the stock market. Do you go see a broker when you have a few thousand bucks laying around you want to invest with?

you can do that or you set one up online, or can call your bank and do it over the phone.

For most people, investing in the stock market is done through your 401(k) or IRA, it is not a separate action. And in fact, dividing these the way the guest poster did — and the way you are reenforcing here — could actually cost someone significant money. You never want to invest in a brokerage account before maxing out your 401(k) and IRA contributions. Otherwise, you’ll lose the very serious tax advantages offered by those accounts. Not pointing this out is really irresponsible.

Also, the line about Traditional IRAs being the best fit for most people simply isn’t true, particularly of the age range I expect reads this blog. Young people actually end to benefit MORE from a Roth IRA, because their time horizon is much longer. However, it’s not a good idea to give a blanket recommendation because every situation is different.

Just like health and fitness advice, financial advice can be pretty tricky to offer to the masses. I would be careful about doing so in the future because while there is some good information here, much of it is too generic to offer much help.

Thanks so much for your comments on the post. I wanted to take an opportunity to respond briefly to a few of your thoughts. I would not recommend anyone invest in stocks only through their 401k, nor would I necessarily recommend that you max out your 401k. However, I would recommend, as I mentioned in the post, that you max out the amount your employer will contribute to your 401K (often 6%).

The key difference between a normal investment account and a 401k is that you cannot withdraw your money from your 401k until you are 59 1/2 without a penalty. If you put all of your savings in your 401k, you will not be able to access any of your savings before retirement (such as in case of emergency or in case you need the money for a big investment like a home). Currently, the max contribution for a 401k is $17,500 a year, and for many of my readers (myself included), that wouldn’t leave enough leftover for savings I could access when I need it in the near future.

Of course, as noted in my disclaimer, no one should implement this advice without considering their personal financial situation. The Day Tradette is based on the premise that investing and taking control of your personal financial situation is empowering for young women, and that everyone can benefit from understanding their options.

I understand the difference. You definitely shouldn’t be putting money you might need in an emergency or to buy a house (or for any other short-term goal) in a 401k, that’s true. But you shouldn’t be investing it, period. The stock market is for long-term savings — savings you won’t need for at least five years, and maybe longer. And you CAN pull contributions out of a Roth IRA without penalty, so it makes a whole lot more sense to use that as a vehicle if you’re worried you may decide you need the money. A brokerage shouldn’t be used until a 401k and/or an IRA is maxed out, otherwise you’re passing up important tax benefits. It just doesn’t make sense to invest in stocks or bonds or any long-term investment in a brokerage instead of a tax-advantaged account.

Well The Day Tradette is about the cutest name for a finance blog I could possibly imagine. Great tips!

Finance majors unite 🙂

*fist bump*

These are great tips! Thankfully I’ve always been financially responsible and did all these things at an early age. I just started dabbling in stocks, but everything else I am well established in. Here’s to retiring early hopefully!

Loved reading this post! Great advice and tips that anyone can start with and relate to.

Being a college student, I am loving all this advice! I am actually super interested in investing, because I know how huge the benefits can be starting at 18. But I suppose I’m just scared of losing it all. This has definitely made me want to do some research, though, and get on it!

These days, I feel like savings accounts are virtually useless! 1% interest? No thanks. I keep a small emergency fund in there because it’s the least risky and very liquid, but I’m an index fund fan for sure! I had some money in a low-risk fund recently for under a year and it grew by about 10%, at which point I had to withdraw for other things. Works for me!!

Totally checking out The Day Tradette. I’m a big nerd and it’s one of my goals to learn more about investing. 🙂

Man, reading his has made me wished that I started a college fund. Weird that my parents never started one.

Vanguard index funds and I are bffs. I love running a lazy portfolio that (tries to) represent the market as a whole.

I think it’s super important women start investing young. Great check in on this. 🙂

(Also, have fun dancing with a giant cranberry Gina!)

Great topic! So glad this was covered and I think it would be really helpful to have even more blog posts about it.

Although out of the fitness and food norm, I think this is a great blog post and it is so important to bring this issue and tips to the surface. I think so many young people are uninformed about saving and what it is going to take to retire down the line. I don’t think you can ever start planning too soon. I already have two retirement funds going but this has made me think about staring an emergency fund. Thanks for the useful tip!

This couldn’t have come at a better time! I’m meeting with a financial advisor in a few weeks 🙂 And I just moved our emergency fund out of our normal checking acct bank and into an account I can’t transfer money out of so easily.

Thank you so much for this post and introducing me to “The Day Tradette”

probably it is worth mentioning that it is very important to check your credit history once a month, or sign up for alerts (Privacy Guard is great), because many people concentrate only on saving/checking accounts, and later find out that some guy used their info, opened a credit card and now they are responsible for it. Sometimes its not only about saving money, but keeping intact and secure what you already have.

that’s an awesome tip. credit monitoring services are very inexpensive, too!

Thanks for sharing! I’m definitely not the best with finances, so these were helpful tips.

One name was a game changer for our finances: Dave Ramsey!

Go through FPU (Financial Peace University), and you will set yourself up for success, and leave an excellent financial legacy for your children. It takes discipline BUT it’s a simple concept and it works. There is no magic pill with finances, just good old fashioned sense. EX: Use cash! When the cash runs out – you are done spending. I know, it’s a scary thought for some people. lol

i’m happy to hear you liked his plan! a friend of mine did it and she said it was awesome, but very challenging

I couldnt agree with you more! He taught us the very, very simple lessons of money. It’s how our grandparents spent their money – lived below their means and didn’t live on credit. In the beginning his plan IS a challenge. Once you are in it, you realize how AWESOME it is and you wouldn’t go back to how you use to live.

I agree with lots of the other commenters — what a fantastic guest post! Very glad to know about The Day Tradette now — I’ll be sure to check her blog out. Thanks for sharing!

I loved this post – lots of great and easy to understand information. I have been considering opening an online trading account to invest in the stock market for awhile and you may have just convinced me. Thanks!

Question for Rachel: Can you suggest any great books that are geared towards women (or anyone for that matter) regarding stocks and investment? From basic to intermediate? My husband is obsessed with stocks and trading (pretty sure we could call it his hobby), so with a psychology background, I’m having a hard time keeping up with everything!! I’ve read a few snoozers, so looking for one that I can get through without it sedating me. Thanks 🙂

Oh and Gina: “example A: I’ll be dancing today by a 60 ft. inflatable cranberry.” You are way too funny.

Hi Kelly,

To be honest I don’t know a ton of books like that. A Random Walk Down Wall Street is a classic, and The Intelligent Investor is a staple written by Warren Buffet’s mentor (but it’s from 1949). I read MotleyFool.com a lot and find it’s very well written. I try to make my website easy to understand for non-finance people so hopefully you can get something out of that as well 🙂

We have the Intelligent Investor… fell asleep to that one! haha

I’ll be sure to swing by your blog. Thanks!

a book that has some great tips and is a lighter read is the millionaire next door, too 🙂

Ah, we have that too! I liked that one, Gina!

Thanks for highlighting Rachel’s blog Gina! I can be a personal finance nerd sometimes so I’m excited to have a new blog to add to my rotation! 😀

Great tips! My husband and I are constantly talking about the best place to put our money away. I can’t wait to show him this post!

Awesome post!!!

I love personal finance! I enjoy reading several personal finance blogs and am glad to see more women taking an active role in their financial futures. I’m a fan of this branching out, Gina!

I would, however, like to point out that recommending a traditional IRA (over a Roth) is backwards from the advice most financial planners would give. I recommend everyone look into this on their own as everyone has a different situation. My personal fav, Suze Orman, has tons of advice on the situation.

love suze orman, too! i’ve read a couple of her books and loved them